The world around us is being disrupted by the acceleration of technology into more industries and more consumer applications. Society is reorienting to a new post-pandemic norm — even before the pandemic itself has been fully tamed. And the loosening of federal monetary policies, particularly in the US, has pushed more dollars into the venture ecosystems at every stage of financing.

We have global opportunities from these trends but of course also big challenges. Technology solutions are now used by authoritarians to monitor and control populations, to stymie an individual company’s economic prospects or to foment chaos through demagoguery. We also have a world that is, as Thomas Friedman so elegantly put it — “Hot, Flat & Crowded.”

With the enormous changes to our economies and financial markets — how on Earth could the venture capital market stand still? Of course we can’t. The landscape is literally and figuratively changing under our feet.

What Has Changed in Financing?

One of the most common questions I’m asked by people intrigued by but also scared by venture capital and technology markets is some variant of, “Aren’t technology markets way overvalued? Are we in a bubble?”

I often answer the same way …

*******

“First, yes, nearly every corner of our market is over-valued. By definition — I’m over-paying for every check I write into the VC ecosystem and valuations are being pushed up to absurd levels and many of these valuations and companies won’t hold in the long term.

However, to be a great VC you have to hold two conflicting ideas in your head at the same time. On the one hand, you’re over paying for every investment and valuations aren’t rational. On the other hand, the biggest winners will turn out to be much larger than the prices people paid for them and this will happen faster than at any time in human history.

So we only need to look at the extreme scaling of companies like Discord, Stripe, Slack, Airbnb, GOAT, DoorDash, Zoom, SnowFlake, CoinBase, Databricks and many others to understand this phenomenon. We operate at scale and speed unprecedented in human history.”

*******

I first wrote about the changes to the Venture Capital ecosystem 10 years ago and this still serves as a good primer of how we arrived at 2011, a decade on from the Web 1.0 dot-com bonanza.

In short, In 2011 I wrote that cloud computing, particularly initiated by Amazon Web Services (AWS)

- Spawned the micro-VC movement

- Allowed a massive increase in the number companies to be created and with fewer dollars

- Created a new breed of LPs focused on very early stage capital (Cendana, Industry Ventures)

- Lowered the age of the average startup and made them more technical

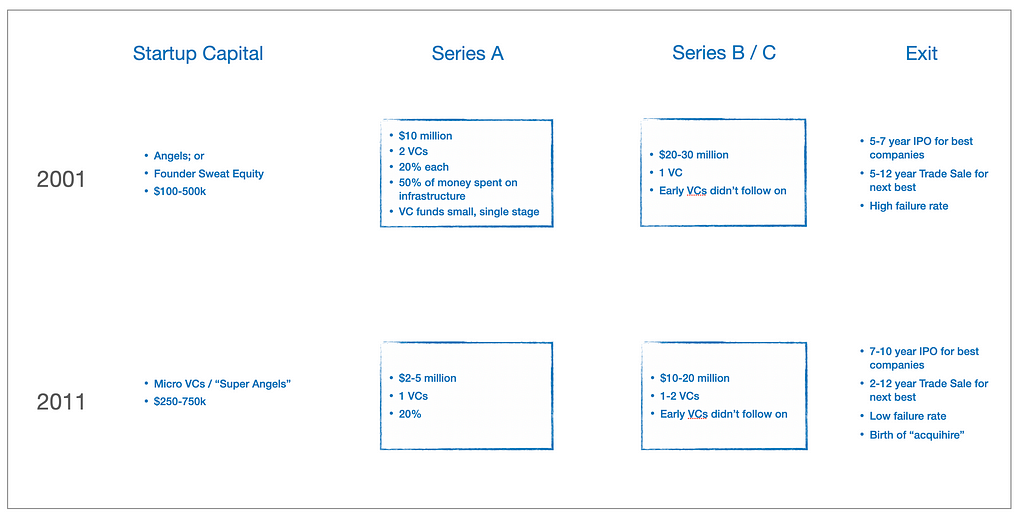

So the main differences in VC between 2001 to 2011 (see graphic above) was that in the former entrepreneurs largely had to bootstrap themselves(except in the biggest froth of the dot com bubble) and by 2011 a healthy micro-VC market had emerged. In 2001 companies IPO’d very quickly if they were working, by 2011 IPOs had slowed down to the point that in 2013 Aileen Lee of Cowboy Ventures astutely called billion-dollar outcomes “unicorns.” How little we all knew how ironic that term would become but has nonetheless endured.

Ten years on much has changed.

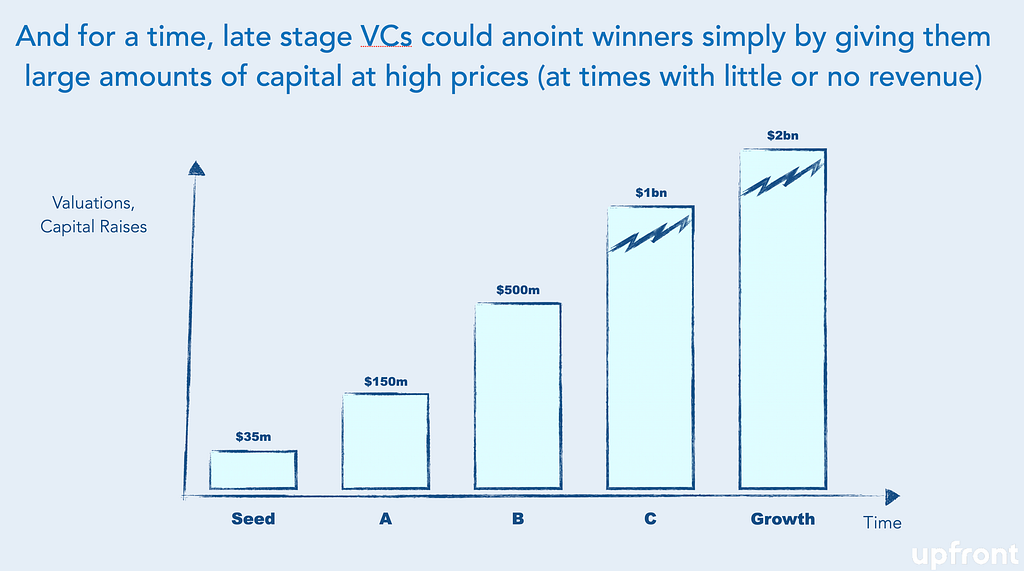

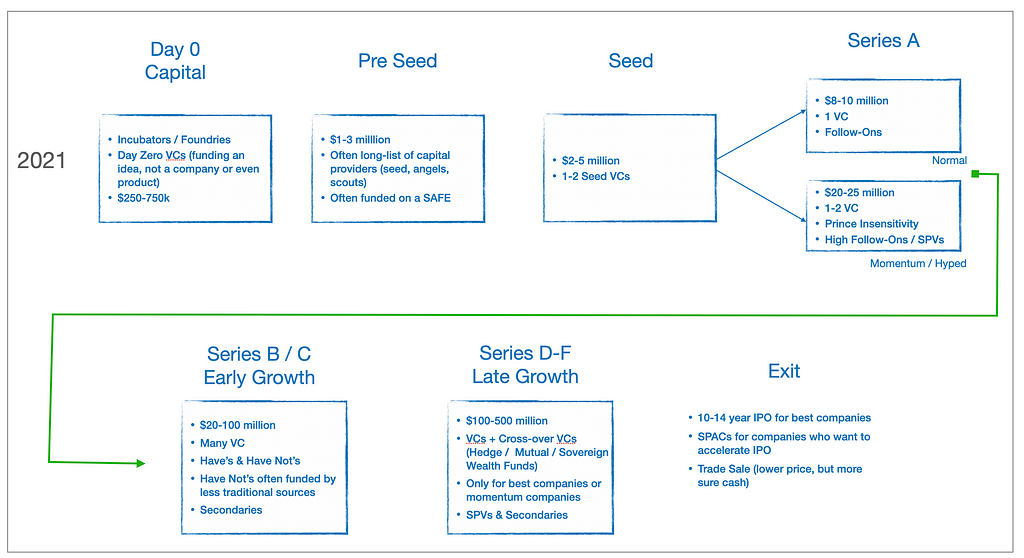

The market today would barely be recognizable by a time traveler from 2011. For starters, a16z was only 2 years old then (as was Bitcoin). Today you have funders focused exclusively on “Day 0” startups or ones that aren’t even created yet. They might be ideas they hatch internally (via a Foundry) or a founder who just left SpaceX and raises money to search for an idea. The legends of Silicon Valley — two founders in a garage — (HP Style) are dead. The most connected and high-potential founders start with wads of cash. And they need it because nobody senior at Stripe, Discord, Coinbase or for that matter Facebook, Google or Snap is leaving without a ton of incentives to do so.

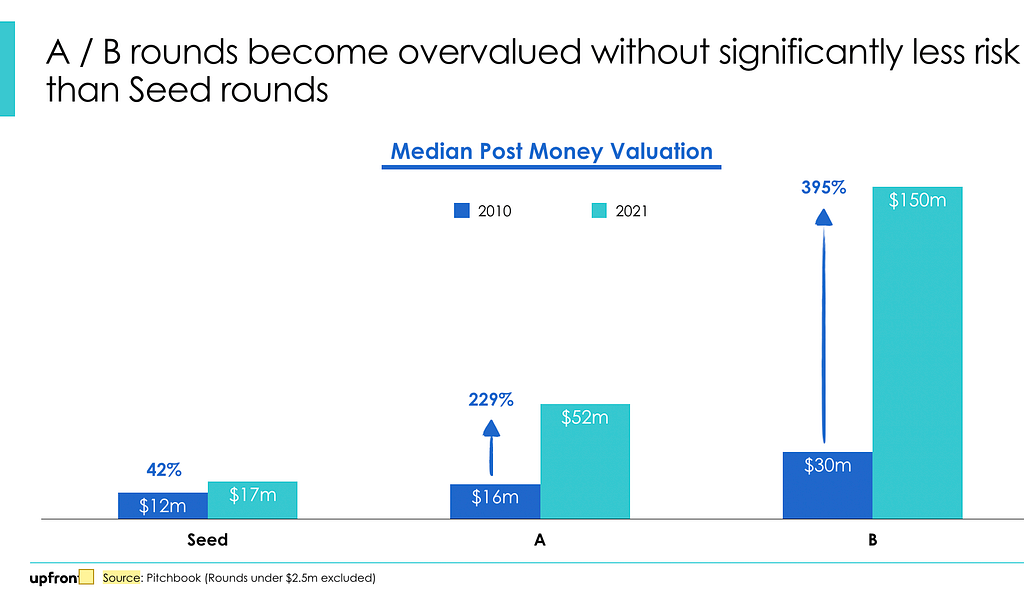

What used to be an “A” round in 2011 is now routinely called a Seed round and this has been so engrained that founders would rather take less money than to have to put the words “A round” in their legal documents. You have seed rounds but you now have “pre-seed rounds.” Pre-seed is just a narrower segment where you might raise $1–3 million on a SAFE note and not give out any board seats.

A seed round these days is $3–5 million or more! And there is so much money around being thrown at so many entrepreneurs that many firms don’t even care about board seats, governance rights or heaven forbid doing work with the company because that would eat into the VCs time needed to chase 5 more deals. Seed has become an option factory for many. And the truth is that several entrepreneurs prefer it this way.

There are of course many Seed VCs who take board seats, don’t over-commit to too many deals and try to help with “company building” activities to help at a company’s vulnerable foundations. So in a way it’s self selecting.

A-Rounds used to be $3–7 million with the best companies able to skip this smaller amount and raise $10 million on a $40 million pre-money valuation (20% dilution). These days $10 million is quaint for the best A-Rounds and many are raising $20 million at $60–80 million pre-money valuations (or greater).

Many of the best exits are now routinely 12–14 years from inception because there is just so much private-market capital available at very attractive prices and without public market scrutiny. And as a result of this there are now very robust secondary markets where founders and seed-funds alike are selling down their ownership long before an ultimate exit.

Our fund (Upfront Ventures) recently returned >1x an entire $200 million fund just selling small minatory in secondary sales while still holding most of our stock for an ultimate public market exits. If we wanted to we could have sold > 2x the fund easily in the secondary markets with significant upside remaining. That never would have happened 10 years ago.

How are VC Firms Like Ours Organizing to Meet the Challenges?

We are mostly running the same playbook we have for the past 25 years. We back very early stage companies and work alongside executive teams as they build their teams, launch their products, announce their companies and raise their first downstream capital rounds. That used to be called A-round investing. The market definition has changed but what we do mostly hasn’t. It’s just now that we’re Seed Investors.

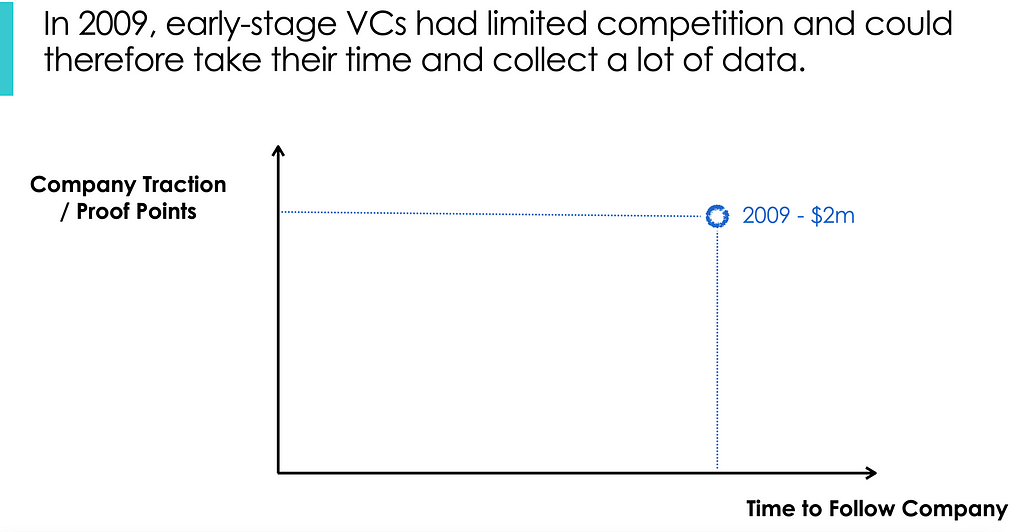

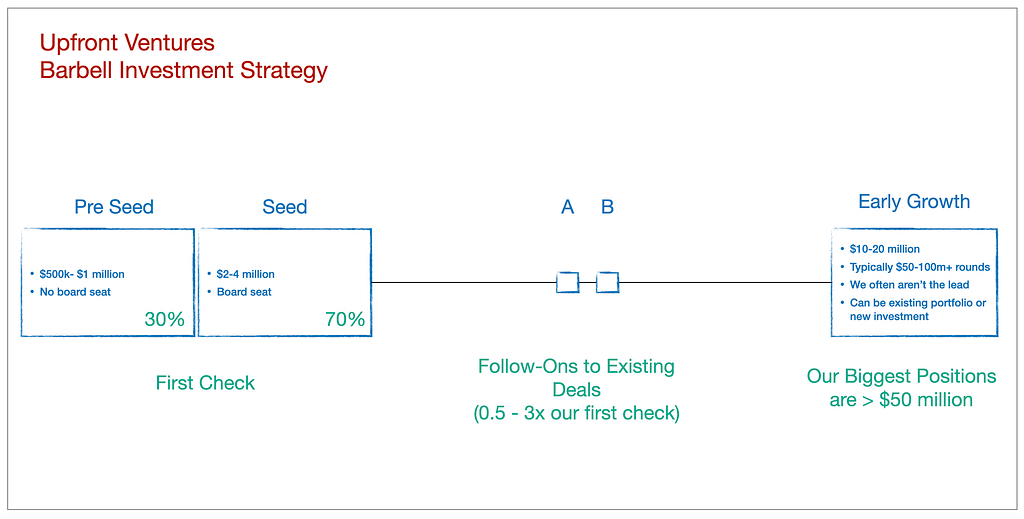

The biggest change for us in early-stage investing is that we now need to commit earlier. We can’t wait for customers to use the product for 12–18 months and do customer interviews or look at purchase cohorts. We have to have strong conviction in the quality of the team and the opportunity and commit more quickly. So in our earliest stages we’re about 70% seed and 30% pre-seed.

We’re very unlikely to do what people now call an “A Round.” Why? Because to invest at a $60–80 million pre-money valuation (or even $40–50 million) before there is enough evidence of success requires a larger fund. If you’re going to play in the big leagues you need to be writing checks from a $700 million — $1 billion fund and therefore a $20 million is still just 2–2.5% of the fund.

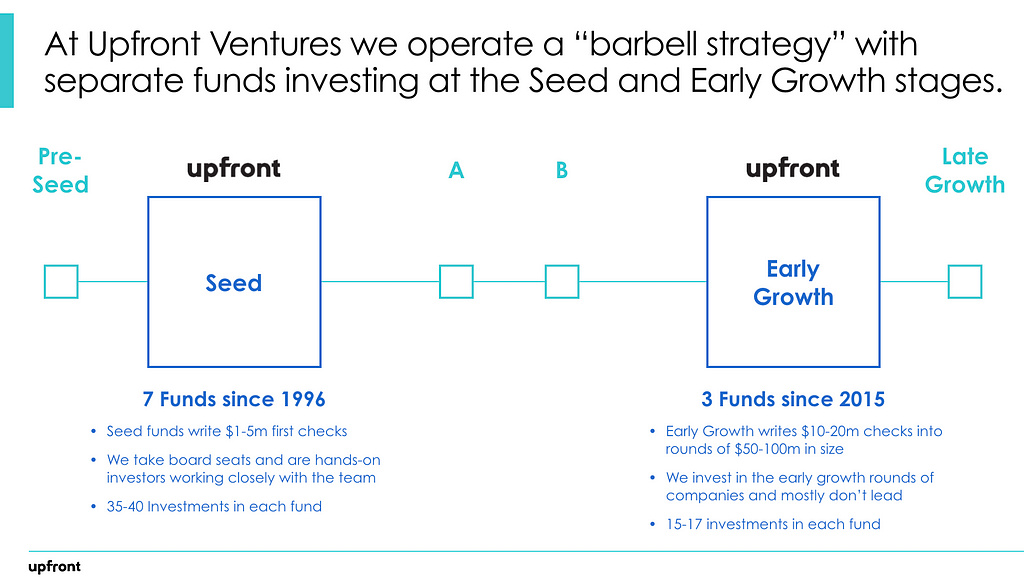

We try to cap our A-funds at around $300 million so we retain the discipline to invest early and small while building our Growth Platform separately to do late stage deals (we now have > $300 million in Growth AUM).

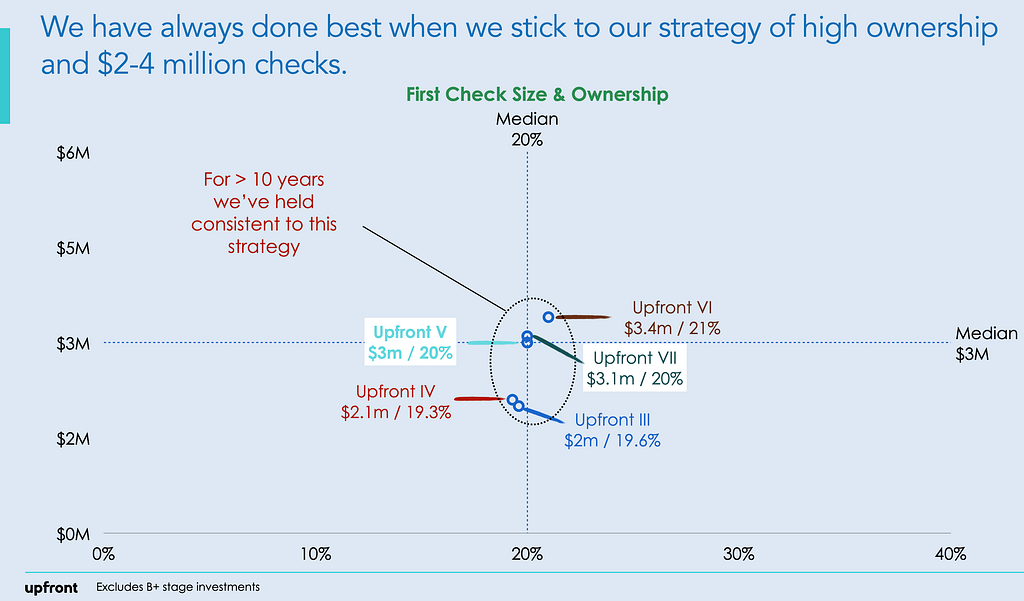

What we promise to entrepreneurs is that if we’re in for $3–4 million and things are going well but you just need more time to prove out your business — at this scale it’s easier for us to help fund a seed extension. These extensions are much less likely at the next level. Capital is a lot less patient at scale.

What we do that we believe is unique relative to some Seed Firms is that we like to think of ourselves as “Seed / A Investors” meaning if we write $3.5 million in a Seed round we’re just as likely to write $4 million in the A round when you have a strong lead.

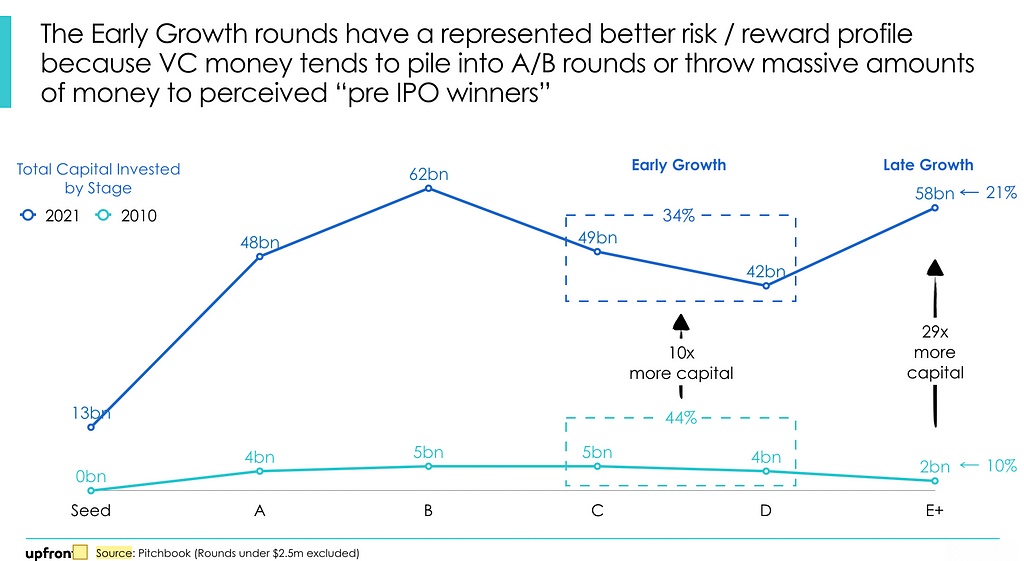

Other than that we’ve adopted a “barbell strategy” where we may choose to avoid the high-priced, less-proven A & B rounds but we have raised 3 Growth Funds that then can lean in when there is more quantitative evidence of growth and market leadership and we can underwrite a $10–20 million round from a separate vehicle.

In fact, we just announced that we hired a new head of our Growth Platform, (follow him on Twitter here → Seksom Suriyapa — he promised me he’d drop Corp Dev knowledge), who along with Aditi Maliwal (who runs our FinTech practice) will be based in San Francisco.

Whereas the skills sets for a Seed Round investor are most tightly aligned with building an organization, helping define strategy, raising company awareness, helping with business development, debating product and ultimately helping with downstream financing, Growth Investing is very different and highly correlated with performance metrics and exit valuations. The timing horizon is much shorter, the prices one pays are much higher so you can’t just be right about the company but you must be right about the valuation and the exit price.

Seksom most recently ran Corporate Development & Strategy for Twitter so he knows a thing or two about exits to corporates and whether he funds a startup or not I suspect many will get value from building a relationship with him for his expertise. Before Twitter he held similar roles at SuccessFactors (SaaS), Akamai (telecoms infrastructure), McAfee (Security Software) and was an investment banker. So he covers a ton of ground for industry knowledge and M&A chops.

If you want to learn more about Seksom you can read his TechCrunch interview here.

What Does this Mean for a Venture Capital Firm?

Years ago Scott Kupor of a16z was telling me that the market would split into “bulge bracket” VCs and specialized, smaller, early-stage firms and the middle ground would be gutted. At the time I wasn’t 100% sure but he made compelling arguments about how other markets have developed as they matured so I took note. He also wrote this excellent book on the Venture Capital industry that I highly recommend → Secrets of Sand Hill Road.

By 2018 I sensed that he was right and we began focusing more on our barbell approach.

We believe that to drive outsized returns you have to have edge and to develop edge you need to spend the preponderance of your time building relationships and knowledge in an area where you have informational advantages.

At Upfront we have always done 40% of our investing in Greater Los Angeles and it’s precisely for this reason. We aren’t going to win every great deal in LA — there are many other great firms here. But we’re certainly focused in an enormous market that’s relatively less competitive than the Bay Area and is producing big winners including Snap, Tinder, Riot Games, SpaceX, GoodRx, Ring, GOAT, Apeel Sciences (Santa Barbara), Scopely, ZipRecruiter, Parachute Home, Service Titan — just to name a few!

But we also organize ourselves around practice areas and have done for the past 7 years and these include: SaaS, Cyber Security, FinTech, Computer Vision, Sustainability, Healthcare, Marketplace businesses, Video Games — each with partners as the lead.

Where are Things Headed for VC in 2031?

Of course I have no crystal ball but if I look at the biggest energy in new company builders these days it seems to me some of the biggest trends are:

- The growth of sustainability and climate investing

- Investments in “Web 3.0” that broadly covers decentralized applications and possibly even decentralized autonomous organizations (which could imply that in the future VCs need to be more focused on token value and monetization than equity ownership models — we’ll see!)

- Investments in the intersection of data, technology and biology. One only needs to look at the rapid response of mRNA technologies by Moderna and Pfizer to understand the potential of this market segment

- Investments in defense technologies including cyber security, drones, surveillance, counter-surveillance and the like. We live in a hostile world and it’s now a tech-enabled hostile world. It’s hard to imagine this doesn’t drive a lot of innovations and investments

- The continued reinvention of global financial services industries through technology-enabled disruptions that are eliminating bloat, lethargy and high margins.

As the tentacles of technology get deployed further into industry and further into government it’s only going to accelerate the number of dollars that pour into the ecosystem and in turn fuel innovation and value creation.

The Changing Venture Landscape was originally published in Both Sides of the Table on Medium, where people are continuing the conversation by highlighting and responding to this story.