Being great as a startup technology investor of course requires a lot of things to come together:

You need to have strong insights into where technology markets are heading and where value in the future will be created and sustained

You need be perfect with your market timing. Being too early is the same as being wrong. Being too late and you back an “also ran”

You also need to be right about the team. If you know the right market and enter at this exact right time you can still miss WhatsApp, Instagram, Facebook, Stripe, etc.

I’ve definitely been wrong on market value. I’ve sometimes been right about the market value but too early. And I’ve been spot on with both but backed the 2nd, 3rd or 4th best player in a market.

In short: Access to great deals, ability to be invited to invest in these deals, ability to see where value in a market will be created and the luck to back the right team with the right market at the right time all matter.

When you first start your career as an investor (or when you first start writing angel checks) your main obsession is “getting into great deals.” You’re thinking about one bullet at a time. When you’ve been playing the game a bit longer or when you have responsibilities at the fund level you start thinking more about “portfolio construction.”

At Upfront we often talk about these as “shots on goal” (a fitting soccer analogy given the EURO 2020 tournament is on right now). What we discuss internally and what I discuss with my LPs is outlined as follows:

We back 36–38 Series Seed / Series A companies per fund (we have a separate Growth Fund)

Our median first check is $3.5 million, and we can write as little as $250k or as much as $15 million in our first check (we can follow on with $50 million + in follow-on rounds)

We build a portfolio that is diversified given the focus areas of our partners. We try to balance deals across (amongst other things): cyber-security, FinTech, computer vision, marketplaces, video games & gaming infrastructure, marketing automation, applied biology & healthcare systems, sustainability and eCommerce. We do other things, too. But these have been the major themes of our partners

We try to have a few “wild, ambitious plans” in every portfolio and a few more businesses that are a new model emerging in an existing sector (video-based online shopping, for example).

We tell our LPs the truth, which is that when we write the first check we think each one is going to be an amazing company but 10–15 years later it has been much hard to have predicted which would be the major fund drivers.

Consider:

When GOAT started it was a restaurant reservation booking app called GrubWithUs … it’s now worth $3.7 billion

We had a portfolio company turn-down a $350 million acquisition because they wanted at least $400 million. They sold 2 years later for $16 million

In the financial crisis of 2008 we had a company that had jointly hired lawyers to consider a bankruptcy and also pursued (and achieved!) the sale of the company for $1 billion. It was ~30 days from bankruptcy.

Almost every successful company is a mixture of very hard work by the founders mixed with a pinch of luck, good fortune and perseverance.

So if you truly want to be great at investing you need all the right skills and access AND a diversified portfolio. You need shots on goal as not every one will go in the back of the net.

The right number of deals will depend on your strategy. If you’re a seed fund that takes 5–10% ownership and doesn’t take board seats you might have 50, 100 or even 200 investments. If you’re a later-stage fund that comes in when there’s less upside but a lower “loss ratio” you might have only 8–12 investments in a fund.

If you’re an angel investor you should figure out how much money you can afford to lose and then figure out how to pace your money over a set period of time (say 2–3 years) and come up with how many companies you think is diversified for you and then back into how many $ to write / company. Hint: don’t do only 2–3 deals!! Many angels I know have signed over more than their comfort level in just 12 months and then feel stuck. It can be years before you start seeing returns.

At Upfront Ventures, we defined our “shots on goal” strategy based on 25 years of experience (we were founded in 1996):

We take board seats and consider ourselves company-builders > stock pickers. So we have to limit the number of deals we do

This drives us to have a more concentrated portfolio, which is why we seek larger ownership where we invest. It means we’re more aligned with the outcomes and successes of the more limited number of deals we do

Across many funds we have enough data to show that 6 or 7 deals will drive 80+% of the returns and a priori we never know which of the 36–38 will perform best.

The outcome of this is that each partner does about 2 new deals per year or 5.5 per fund. We know this going into a new fund.

So each fund we’re really looking for 1–2 deals that return $300 million+ on just one deal. That’s return, not exit price of the company. Since our funds are around $300 million each this returns 2–4x the fund if we do it right. Another 3–5 could return in aggregate $300–500 million. The remaining 31 deals will likely return less than 20% of all returns. Early-stage venture capital is about extreme winners. To find the right 2 deals you certainly need a lot of shots on goal.

We have been fortunate enough to have a few of these mega outcomes in every fund we’ve ever done.

In a follow-up post I’ll talk about how we define how many dollars to put into deals and how we know when it’s time to switch from one fund to the next. In venture this is called “reserve planning.”

I recently wrote a post about funding for investors to think about having a diversified portfolio, which I called “shots on goal.” The thesis is that before investing in an early-stage startup it is close to impossible to know which of the deals you did will break out to the upside. It’s therefore important to have enough deals in your program to allow for the 15–20% of amazing deals to emerge. If you funded 30–40 deals perhaps just 1 or 2 would drive the lion’s shares of returns.

You can think of a shot on goal as the numerator in a fraction where the numerator is the actual deals you completed and the denominator is the total number of deals that you saw. In our funds we do about 12 deals / year and see several thousand so the funding rate is somewhere between 0.2–0.5% of deals we evaluate depending on how you count what constitutes “evaluating a deal.”

This is Venture Capital.

The Denominator Effect

I want to share with you some of the most consistent pieces of advice I give to new VCs in their career journey and the same advice holds for angel investors. Focus a lot on the denominator.

Let’s assume that you’re a reasonably well-connected person, you have a strong network of friends & colleagues who work in the technology sector and you have many friends who are investors either professionally or as individuals.

Chances are you’ll see a lot of good deals. I’d be willing to bet that you’d even see a lot of deals that seem amazing. In the current market it’s not that hard to find executives leaving: Facebook, Google, Airbnb, Netflix, Snap, Salesforce.com, SpaceX … you name it — to start their next company. You’ll find engineers out of MIT, Stanford, Harvard, UCSD, Caltech or execs out of UCLA, Spelman, NYU, etc. The world of talented people from the top companies & top schools is literally tens of thousands of people.

And then add on to this people who worked at McKinsey, BCG, Bain, Goldman Sachs, Morgan Stanley and what you’ll have is not only really ambitious young talent but also people great at doing presentation decks filled with data and charts and who have perfected the art of narrative storytelling through data and forecasts.

Now let’s assume you take 10 meetings. If you’re reasonably smart and thoughtful and hustle to get in front great teams I feel highly confident you’ll find at least 3 of them compelling. If you get in front of great teams, how could you not?

But now let’s assume that you push yourself hard to see 100 deals over a 90 day period and meet as many teams as you can and don’t necessarily invest in any of them but you’re patient to see what great truly looks like. I feel confident that after seeing 100 companies you’ll have 4 or 5 that really stand out and you find compelling.

But here’s the rub — almost certainly there will be no overlap from those first three deals you thought were high quality and the 4 or 5 you’re now ready to pound your fist on the table to say you should fund.”

Ok, but the thought experiment needs to be expanded. Now let’s say you took an entire year and saw 1,000 companies. There is no way you’d be advocating to fund 300–400 hundred of them (the same ratio as the 3–4 out of your first 10 deals). In all likelihood 7 or 8 deals would really stand out as truly exceptional, MUST DO, slam-your-first-on-the-table type deals. And of course the 7 or 8 deals would be different from the 4 or 5 you first saw and were ready to fight for.

Venture is a numbers game. So is angel investing. You need to see a ton of deals to begin to distinguish good from great and great from truly exceptional. If your denominator is too low you’ll fund deals you consider compelling at the time that wouldn’t pass muster with your future self.

So my advice boils down to these simple points:

Make sure you see tons of deals. You need to develop pattern recognition for what truly exceptional looks like.

Don’t rush to do deals. Almost certainly the quality of your deal flow will improve over time as will your ability to distinguish the best deals

I also am personally a huge fan of focus. If you see a FinTech deal today, a Cyber Security deal tomorrow and then creator tools the next day … it’s harder to see the pattern and have the knowledge of truly exceptional is. If you see every FinTech company you can possible meet (or even a sub-sector of FinTech like Insurance Tech company … you can truly develop both intuition and expertise over time).

Get lots of shots on goal (completed deals, which is the numerator) in order to build a diversified portfolio. But make sure your shots are coming from a very large pool of potential deals (the denominator) to have the best chances of success.

Customer acquisition is the lifeblood of many startups from e-commerce to gaming to marketplace companies, among others. Most of these startups spend the lion’s share of their marketing budget in today’s social media channels: Facebook, Twitter, Reddit, Snap, TikTok and so on because — no surprise — that’s where the customers are.

Digital advertising spend is projected to grow 25% this year to $191 billion, and Google (69%), Facebook (59%), Snapchat (116%) and Twitter (87%) all just reported rapid growth in their year over year advertising revenues. For these companies, it looks like a rosy picture.

But if you ask anyone in the ecosystem of customer acquisition — founders, marketers, investors — and you’ll hear the same thing: customer acquisition (CAC) is getting harder and more expensive. Some of this can be attributed to the exponential growth in e-commerce and direct-to-consumer businesses as a result of the pandemic and global lockdowns — eCommerce for example grew 39% just last year – so there’s simply more demand. And some of this can be attributed to the increased pressure on the available platforms not only to facilitate acquisition at scale but to do so in an increasingly “walled garden,” privacy-restricted world.

Despite the huge and sustained growth in digital advertising (or maybe because of it), there are virtually no tools where a marketer or growth leader can understand their performance and spend across channels, nor where they can share best practices and insights with their peers so the platforms are at an information advantage.

That’s where Trust comes in — it was built to arm those spending money in channels in order not to be at a disadvantage.

Trust, which today has announced a $9 million financing (Upfront is an investor), is a platform designed to help make the most of marketing investment by providing both analytics and a community of likeminded executives to share what’s working, and what’s not, across platforms. Think of it as Bloomberg for marketers, in a way that gives smaller companies and teams as much firepower as larger organizations to help them optimize spend across channels and identify new, high-performing opportunities. This is accomplished through aggregated, anonymized competitive benchmarking, market-level performance data across the major social and ad platforms, and curated news and conversation from industry leaders.

To start, Trust is also launching with the Trust virtual card, which essentially funnels credits and preferred billing to any business, allowing them to increase their marketing buying power by up to 20x and receive 45-day payment terms for all their marketing investments.

Why Did I Invest in Trust?

As a VC, one of the key things I’m looking for in any new investor is “product-founder fit” e.g. does this founder have an insight or advantage that makes them uniquely suited to successfully build this product and business? There are plenty of talented, smart founders out there but you’d be surprised how many don’t have that “unfair advantage” when it comes to their product and audience.

Trust is led by CEO and co-founder James Borow, who led Snap’s global programmatic ads platform and grew the self-service ads revenue from 0 to $1B+ over three years. In that role, James and his co-founders (many also from the Snap team) saw first-hand how hard it was for companies to understand where and how to best invest in marketing, and how opaque the platforms make it for advertisers. They lived this challenge every day alongside their customers at Snap, and Trust was founded out of a direct desire to reshape marketing and ad-spend dynamics for the people who are on the ground building businesses. To me, that’s the textbook example of “product-founder fit” and one of the reasons I believe this business will succeed.

Since day one I’ve believed in James as a founder who deeply understands and empathizes with his customer pain point, not just from the user side but also from the platform side. A lot of people have tried to solve multi-channel analytics and optimization, but I believe James and team have the unique set of skills and experience to finally crack the code.

As an investor in early-stage companies, many of whom are living the customer acquisition challenge every day, I’m excited to see how Trust can reshape the playing field for startups and larger organizations alike. Founders, marketers and growth leaders — join the Trust waitlist here.

The world around us is being disrupted by the acceleration of technology into more industries and more consumer applications. Society is reorienting to a new post-pandemic norm — even before the pandemic itself has been fully tamed. And the loosening of federal monetary policies, particularly in the US, has pushed more dollars into the venture ecosystems at every stage of financing.

We have global opportunities from these trends but of course also big challenges. Technology solutions are now used by authoritarians to monitor and control populations, to stymie an individual company’s economic prospects or to foment chaos through demagoguery. We also have a world that is, as Thomas Friedman so elegantly put it — “Hot, Flat & Crowded.”

With the enormous changes to our economies and financial markets — how on Earth could the venture capital market stand still? Of course we can’t. The landscape is literally and figuratively changing under our feet.

What Has Changed in Financing?

One of the most common questions I’m asked by people intrigued by but also scared by venture capital and technology markets is some variant of, “Aren’t technology markets way overvalued? Are we in a bubble?”

I often answer the same way …

*******

“First, yes, nearly every corner of our market is over-valued. By definition — I’m over-paying for every check I write into the VC ecosystem and valuations are being pushed up to absurd levels and many of these valuations and companies won’t hold in the long term.

However, to be a great VC you have to hold two conflicting ideas in your head at the same time. On the one hand, you’re over paying for every investment and valuations aren’t rational. On the other hand, the biggest winners will turn out to be much larger than the prices people paid for them and this will happen faster than at any time in human history.

So we only need to look at the extreme scaling of companies like Discord, Stripe, Slack, Airbnb, GOAT, DoorDash, Zoom, SnowFlake, CoinBase, Databricks and many others to understand this phenomenon. We operate at scale and speed unprecedented in human history.”

*******

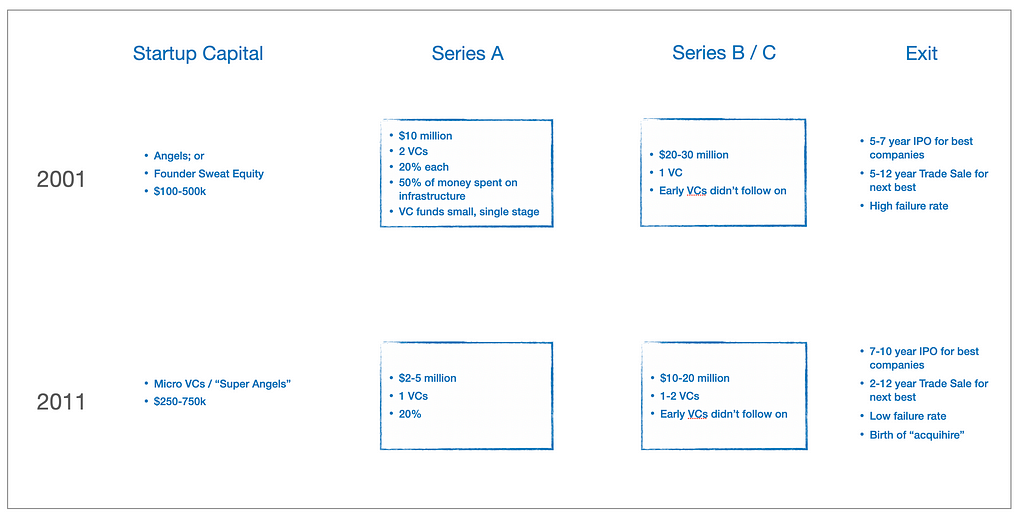

I first wrote about the changes to the Venture Capital ecosystem 10 years ago and this still serves as a good primer of how we arrived at 2011, a decade on from the Web 1.0 dot-com bonanza.

In short, In 2011 I wrote that cloud computing, particularly initiated by Amazon Web Services (AWS)

Spawned the micro-VC movement

Allowed a massive increase in the number companies to be created and with fewer dollars

Created a new breed of LPs focused on very early stage capital (Cendana, Industry Ventures)

Lowered the age of the average startup and made them more technical

So the main differences in VC between 2001 to 2011 (see graphic above) was that in the former entrepreneurs largely had to bootstrap themselves(except in the biggest froth of the dot com bubble) and by 2011 a healthy micro-VC market had emerged. In 2001 companies IPO’d very quickly if they were working, by 2011 IPOs had slowed down to the point that in 2013 Aileen Lee of Cowboy Ventures astutely called billion-dollar outcomes “unicorns.” How little we all knew how ironic that term would become but has nonetheless endured.

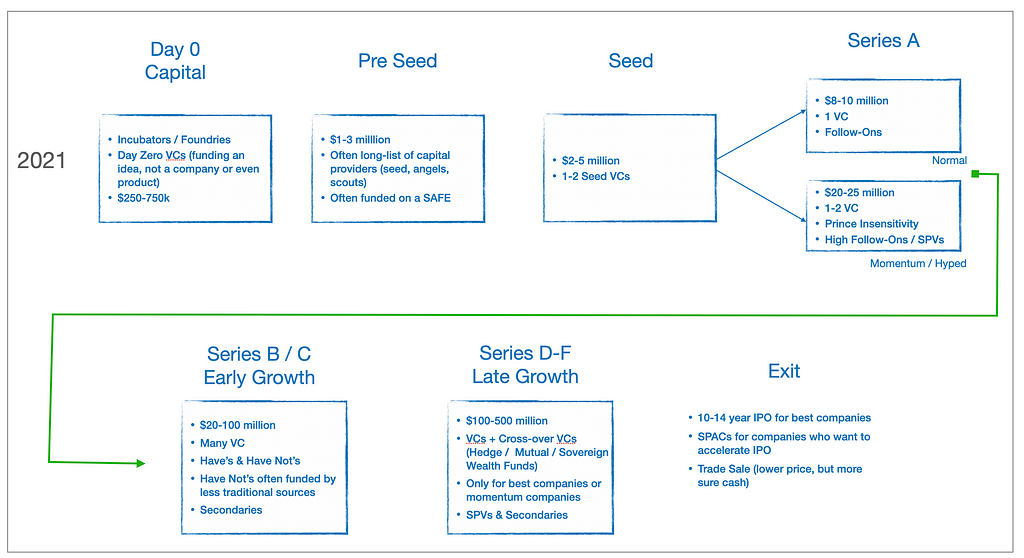

Ten years on much has changed.

The market today would barely be recognizable by a time traveler from 2011. For starters, a16z was only 2 years old then (as was Bitcoin). Today you have funders focused exclusively on “Day 0” startups or ones that aren’t even created yet. They might be ideas they hatch internally (via a Foundry) or a founder who just left SpaceX and raises money to search for an idea. The legends of Silicon Valley — two founders in a garage — (HP Style) are dead. The most connected and high-potential founders start with wads of cash. And they need it because nobody senior at Stripe, Discord, Coinbase or for that matter Facebook, Google or Snap is leaving without a ton of incentives to do so.

What used to be an “A” round in 2011 is now routinely called a Seed round and this has been so engrained that founders would rather take less money than to have to put the words “A round” in their legal documents. You have seed rounds but you now have “pre-seed rounds.” Pre-seed is just a narrower segment where you might raise $1–3 million on a SAFE note and not give out any board seats.

A seed round these days is $3–5 million or more! And there is so much money around being thrown at so many entrepreneurs that many firms don’t even care about board seats, governance rights or heaven forbid doing work with the company because that would eat into the VCs time needed to chase 5 more deals. Seed has become an option factory for many. And the truth is that several entrepreneurs prefer it this way.

There are of course many Seed VCs who take board seats, don’t over-commit to too many deals and try to help with “company building” activities to help at a company’s vulnerable foundations. So in a way it’s self selecting.

A-Rounds used to be $3–7 million with the best companies able to skip this smaller amount and raise $10 million on a $40 million pre-money valuation (20% dilution). These days $10 million is quaint for the best A-Rounds and many are raising $20 million at $60–80 million pre-money valuations (or greater).

Many of the best exits are now routinely 12–14 years from inception because there is just so much private-market capital available at very attractive prices and without public market scrutiny. And as a result of this there are now very robust secondary markets where founders and seed-funds alike are selling down their ownership long before an ultimate exit.

Our fund (Upfront Ventures) recently returned >1x an entire $200 million fund just selling small minatory in secondary sales while still holding most of our stock for an ultimate public market exits. If we wanted to we could have sold > 2x the fund easily in the secondary markets with significant upside remaining. That never would have happened 10 years ago.

How are VC Firms Like Ours Organizing to Meet the Challenges?

We are mostly running the same playbook we have for the past 25 years. We back very early stage companies and work alongside executive teams as they build their teams, launch their products, announce their companies and raise their first downstream capital rounds. That used to be called A-round investing. The market definition has changed but what we do mostly hasn’t. It’s just now that we’re Seed Investors.

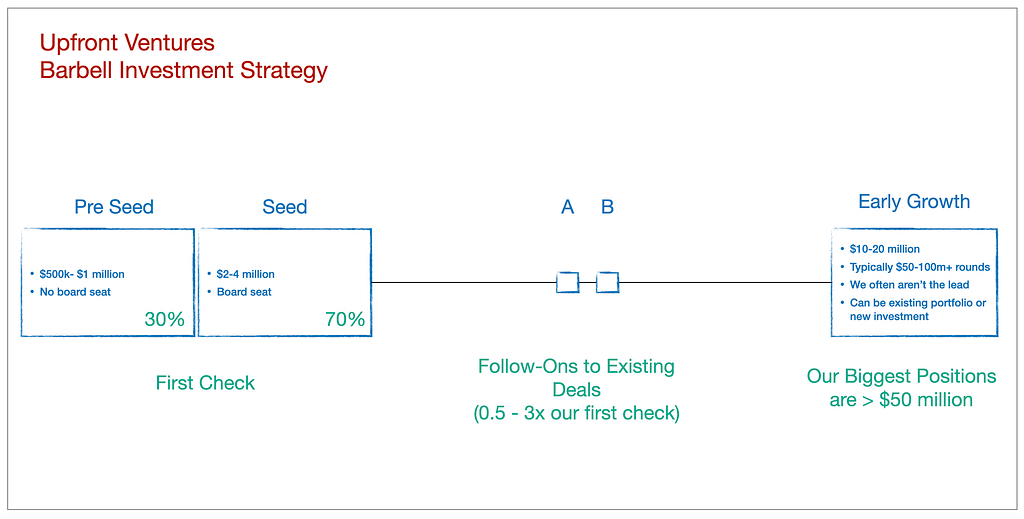

The biggest change for us in early-stage investing is that we now need to commit earlier. We can’t wait for customers to use the product for 12–18 months and do customer interviews or look at purchase cohorts. We have to have strong conviction in the quality of the team and the opportunity and commit more quickly. So in our earliest stages we’re about 70% seed and 30% pre-seed.

We’re very unlikely to do what people now call an “A Round.” Why? Because to invest at a $60–80 million pre-money valuation (or even $40–50 million) before there is enough evidence of success requires a larger fund. If you’re going to play in the big leagues you need to be writing checks from a $700 million — $1 billion fund and therefore a $20 million is still just 2–2.5% of the fund.

We try to cap our A-funds at around $300 million so we retain the discipline to invest early and small while building our Growth Platform separately to do late stage deals (we now have > $300 million in Growth AUM).

What we promise to entrepreneurs is that if we’re in for $3–4 million and things are going well but you just need more time to prove out your business — at this scale it’s easier for us to help fund a seed extension. These extensions are much less likely at the next level. Capital is a lot less patient at scale.

What we do that we believe is unique relative to some Seed Firms is that we like to think of ourselves as “Seed / A Investors” meaning if we write $3.5 million in a Seed round we’re just as likely to write $4 million in the A round when you have a strong lead.

Other than that we’ve adopted a “barbell strategy” where we may choose to avoid the high-priced, less-proven A & B rounds but we have raised 3 Growth Funds that then can lean in when there is more quantitative evidence of growth and market leadership and we can underwrite a $10–20 million round from a separate vehicle.

In fact, we just announced that we hired a new head of our Growth Platform, (follow him on Twitter here → Seksom Suriyapa — he promised me he’d drop Corp Dev knowledge), who along with Aditi Maliwal (who runs our FinTech practice) will be based in San Francisco.

Whereas the skills sets for a Seed Round investor are most tightly aligned with building an organization, helping define strategy, raising company awareness, helping with business development, debating product and ultimately helping with downstream financing, Growth Investing is very different and highly correlated with performance metrics and exit valuations. The timing horizon is much shorter, the prices one pays are much higher so you can’t just be right about the company but you must be right about the valuation and the exit price.

Seksom most recently ran Corporate Development & Strategy for Twitter so he knows a thing or two about exits to corporates and whether he funds a startup or not I suspect many will get value from building a relationship with him for his expertise. Before Twitter he held similar roles at SuccessFactors (SaaS), Akamai (telecoms infrastructure), McAfee (Security Software) and was an investment banker. So he covers a ton of ground for industry knowledge and M&A chops.

Years ago Scott Kupor of a16z was telling me that the market would split into “bulge bracket” VCs and specialized, smaller, early-stage firms and the middle ground would be gutted. At the time I wasn’t 100% sure but he made compelling arguments about how other markets have developed as they matured so I took note. He also wrote this excellent book on the Venture Capital industry that I highly recommend → Secrets of Sand Hill Road.

By 2018 I sensed that he was right and we began focusing more on our barbell approach.

We believe that to drive outsized returns you have to have edge and to develop edge you need to spend the preponderance of your time building relationships and knowledge in an area where you have informational advantages.

At Upfront we have always done 40% of our investing in Greater Los Angeles and it’s precisely for this reason. We aren’t going to win every great deal in LA — there are many other great firms here. But we’re certainly focused in an enormous market that’s relatively less competitive than the Bay Area and is producing big winners including Snap, Tinder, Riot Games, SpaceX, GoodRx, Ring, GOAT, Apeel Sciences (Santa Barbara), Scopely, ZipRecruiter, Parachute Home, Service Titan — just to name a few!

But we also organize ourselves around practice areas and have done for the past 7 years and these include: SaaS, Cyber Security, FinTech, Computer Vision, Sustainability, Healthcare, Marketplace businesses, Video Games — each with partners as the lead.

Where are Things Headed for VC in 2031?

Of course I have no crystal ball but if I look at the biggest energy in new company builders these days it seems to me some of the biggest trends are:

The growth of sustainability and climate investing

Investments in “Web 3.0” that broadly covers decentralized applications and possibly even decentralized autonomous organizations (which could imply that in the future VCs need to be more focused on token value and monetization than equity ownership models — we’ll see!)

Investments in the intersection of data, technology and biology. One only needs to look at the rapid response of mRNA technologies by Moderna and Pfizer to understand the potential of this market segment

Investments in defense technologies including cyber security, drones, surveillance, counter-surveillance and the like. We live in a hostile world and it’s now a tech-enabled hostile world. It’s hard to imagine this doesn’t drive a lot of innovations and investments

The continued reinvention of global financial services industries through technology-enabled disruptions that are eliminating bloat, lethargy and high margins.

As the tentacles of technology get deployed further into industry and further into government it’s only going to accelerate the number of dollars that pour into the ecosystem and in turn fuel innovation and value creation.

Nearly six years ago, I was thrilled to invest in Andrew Farah and the team at Density when they had a vision for building anonymous tracking of how people use office buildings, rentals and other public spaces.

And today, as the company announces their latest funding round of $125M at a $1B+ valuation, I’m still thrilled to back Density as they are growing massively with customers like Uber, Shopify, Delta, and Cisco, among many others. Quite simply, the data that Density provides — data that hasn’t been available until now — is changing the way companies, real estate leaders and employees think about and measure these major assets.

I’m excited to share a short conversation with Andrew about today’s news and where the company is going, which you can see here:

We cover:

Density’s growth and transition through the past two years of a pandemic where — turns out! — knowing where people are in proximity, without violating their privacy, is pretty important